The Butterfly Effect

Election nights’ shocks in France

The unprecedented number of elections around the world and the number of people affected was one of the most flagged risks of 2024. Countries accounting for 45% of the world population held elections in 2024, the highest ratio since 1800 (Deutsche Bank data). Six of the seven G7 countries will hold important elections before October 2025.

Financial markets are often defined as discounting mechanisms. But how well does the discounting work? In the space of just three weeks, elections in India, Mexico, and the European Union have returned a surprise in India and two “as expected” outcomes in Mexico and France.

However, the much-expected first place in the election to the European Parliament obtained by Marine Le Pen’s Rassemblement National (RN) in France led to a very unexpected snap parliamentary election which has resulted in a widening of French Government bond spreads and a correction in the French stock market.

Tonight, early polls suggest a victory for the Nouveau Front Populaire (NFP), a coalition of left wing parties and a resounding defeat for RN, last week’s first round victor. Constructive analysts look to a possible majority formed by President Macron’s party in coalition with the Socialists and the Greens. However, we are afraid that Jean Luc Melonchon’s France Insoumise voters, who believe to have won the election, will take to the streets and paralyse the country. As it turns out, the “useful” vote also comes at a price of governability.

The Fiscal Conundrum

Two out France’ three largest political parties are tagged extreme right and extreme left by journalists and commentators. Like all populist movements, they share a disregard for fiscal consolidation. On the contrary, both parties have large spending plans.

RN plans to raise taxes on the affluent while lowering VAT on household essentials and energy. The communist inspired party would fund an additional €100 billion in spending by squeezing the rich, reintroducing a wealth tax and estate taxes. However, analysts doubt these measures will raise much revenue.

Sadly, the best-case scenario for France’s government debt is a Macron party victory, which will lead to several more years with a fiscal deficit of 4% of GDP.

Will the euro woes resurface?

The market wobbles that may follow an extremist party victory, or a hung parliament, will test the resolve of European politicians and the European Central Bank to hold up the euro together once again. This time around, it may well be more difficult as the debt ceiling and budget rules have been ignored for years, and the central banks with creditor positions in the euro system may feel they do not have enough firepower to buttress France together with the rest of the periphery.

In the European Parliament, the European Popular Party (EPP) together with their traditional allies the Socialists & Democrats (S&D) need the support of other parties to pass legislation as they are well short of a majority. They are very likely to get that support from Renew Europe, a new liberal pro-integration party.

The European Conservatives and Reformists, the third largest party in the chamber, are soft Eurosceptics and anti-federalists. Together with the more right-wing Identity and Democracy, these two parties’ combined forces result in a larger number of European MPs than the Socialists: 141 vs. 136. However, the risk remains that there might be enormous difficulties in pushing a federal agenda through the national parliaments of the more Eurosceptic countries today.

This time is different

While some analysts expect a replay of the euro area Sovereign and Banking crises, and are therefore taking out the old playbook, we believe there are a number of reasons why this time is different.

The Eurosystem of euro area central banks is suffering large losses inherited from Quantitative Easing.

Euro area central banks are reeling from the losses on the carry on their large government bond positions. The 2023 financial statements for the Bundesbank illustrate this well. Currently, almost all euro area sovereign bonds have a negative carry vs de ECB’s deposit rate. Obviously, this problem will disappear with lower policy rates.

However, the “there is no free lunch rule” would still apply as a significant drop in rates in the euro area would lead to a further depreciation of the euro that may result in higher inflation. In addition, lower rates will quickly dent the profitability of euro area banks creating a potential new source of problems, especially if these banks suffer losses on their government bond portfolios, which are currently overweight Italy and Spain.

In 2023, the Bundesbank reported negative net interest income (NII) of €13.9 billion. This shocking result as euro area banks were posting record high NIIs was obtained thanks to a positive net interest income in foreign currency of €1.9bn, as the loss in the euro positions amounted to €15.8billion. The Bundesbank’s long-dated bond portfolio yielded just 37 basis points at cost, while the average interest paid on monetary policy deposits for the year rose to 3.27%. In addition, the Bundesbank’s share in the ECB asset purchase schemes, the Public Sector Purchase Programme (PSPP) and the Pandemic Emergency Purchase Programme (PEPP), resulted in financing charges of €5.2bn. The operating income after staff expense for 2023 is a loss of €21.6 billion. These losses were covered with the release of reserves which have dropped to just €700 million to cover further unexpected risks in a €2.5 trillion balance sheet, the equivalent of 62.5% of German GDP!

Dr Sabine Mauderer, member of the Bundesbank Executive Board, ends her review of the financial performance with a stark conclusion:

“The financial burdens are high. And we are expecting them to be considerable again in 2024. Overall, we are assuming that we will have to work with loss carry-forwards for some time and therefore be unable to distribute any profits for a longer period. As you know, it won’t be the first time the Bundesbank carries losses forward. That happened back in the 1970s as well. Back then, the net accumulated losses were offset by subsequent profits, and the same can be done in the current situation.

I’d like to conclude my remarks with the most important message for today:

The Bundesbank has considerable assets, which are significantly in excess of its obligations. Our revaluation reserves, for instance, amount to almost €200 billion.

In short, the Bundesbank can bear these financial burdens. The Bundesbank’s balance sheet is sound.”

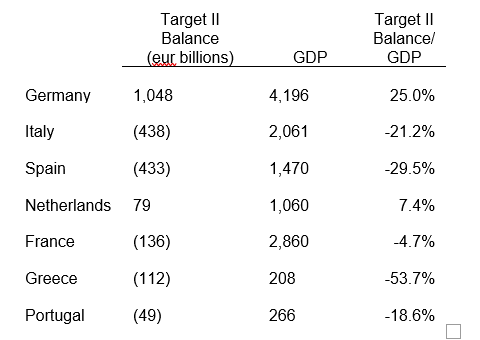

Some Good News from Target 2 Exposure

A rare source of good news in this brewing crisis is the fact that Target 2 exposures are well below their highs post euro area sovereign and banking crises. While this may well prove to be a source of flexibility, new rules need to be devised as euro member countries that stray from the fiscal rules are not eligible for the ECB to support their government bonds’ spreads.

Government debt is not the sole concern around French finances

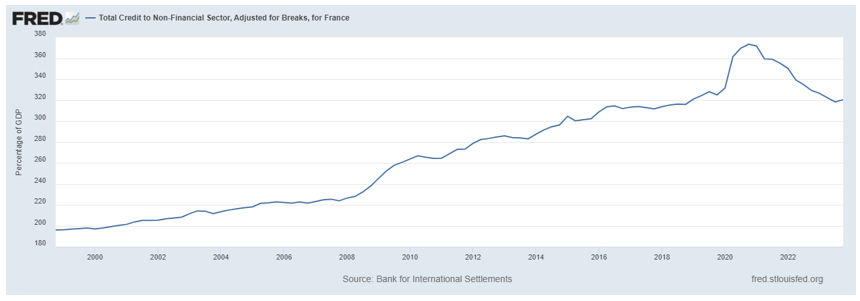

We have regularly expressed concerns for some time regarding France’s twin deficits, complex domestic politics, and slow growth. These are a very poor backdrop for one of the most indebted economies in the world. While most economists are focusing on France’s fiscal deficit path and government debt to GDP, we also worry about the overall leverage in a slow growing economy. As of December 2023, total credit to the non-financial sector stands at 320.4% of GDP in France.

Unlike in 2010, France today has a negative net international investment position

According to EUROSTAT, France’s net international investment position in December 2023 is -29.40%, which means that France owes close to 30% of its GDP to non-resident investors. As of the latest figures published by Agence France Trésor (December 2023) non-residents hold 53.2% of the total negotiable French Government Bonds (OATs) outstanding. We note that all French Government bonds have a negative carry vs repo rates currently.

A new Crisis comes with government debt is at record highs and a best-case scenario with structural large fiscal deficits

Fiscal profligacy is the political boon of our times. Since COVID, politicians the world over have rediscovered the joys of buying votes and how fiscal deficits in the short term do not seem to matter very much. However, the National Rally’s platform calls for tax cuts that would add close to 4% of GDP to France’s already large twin deficits of 9.4 of GDP. Spain and Italy’s are slightly higher at 9.6 and 9.8% of GDP respectively. Conversely, The Netherlands and Germany have twin surpluses of 12.8 and 7.2% of GDP.

French Government bonds have repriced to Spain’s spread levels. There is a higher probability of a second euro area sovereign debt crisis, perhaps followed by a banking crisis.

France, a nuclear power, is no pushover. Will France, the Church’s eldest daughter, become the mother of a Catholic euro?

France is unlikely to yield to pressure in the manner in which Greece, Portugal, or Spain conducted their fiscal consolidation, financial sector restructuring, and internal devaluations. Also, note that France has not run a budget surplus since 1974.

Gideon Rachman of the Financial Times expresses the conventional wisdom among political and financial analysts, “At best, a parliament dominated by these extremist parties may lead to a period of political instability. At worst, it would lead to the adoption of spendthrift and nationalistic policies that would swiftly provoke an economic and social crisis in France”. Traditional politicians also worry about a potential debt crisis.

However, we believe that these analysts are misguided in believing that the IMF or the European Commission would have the ability or the firepower to supervise France’s finances for a debt crisis there will highlight that these institutions are not prepared to assist such a large economy.

The Troika was able to provide financial assistance to Greece, Portugal, and Spain in a sequential manner whereby Spain contributed to the funding of Greece and Portugal until soon after it received its own programme moneys. It is difficult to see a scenario whereby France would be the only country needing a package. We would expect Italy, Spain and Portugal to be dragged into the maelstrom as well. This leaves Germany and The Netherlands to sort out the new crisis on their own. The combined economic and financial sector weights of the problem countries may be too big to fail and too big to rescue.

The euro has not delivered on its promise, especially on growth

There is also an existential problem behind these woes. The stark reality is that the euro has not lived up to its avowed potential. GDP growth has trailed the US’s, and it has not brought either price or financial stability.

The EU is still very far from working efficiently as a single market. Regulatory capture in many industries has prevented the healthy competition and economies of scale envisioned by the euro’s proponents.

The European Commission, a very large and powerful bureaucracy led by former politicians, has created a business unfriendly administrative state, which is intent on becoming the regulator to the world.

There is a broad political consensus supporting the green agenda, which only proximate outcome are hundreds of billions of euros of very low or negative return renewable energy projects and the huge costs imposed on various industries to meet regulatory targets. All policy papers seem to embrace as a crucial target what has so far proven to be a drag on growth and innovation, and a strategic blunder for energy security.

Mario Draghi has become the go-to person when European politicians cannot solve big problems. He rescued the euro by breaking the currency block’s rules. Today, he is in charge of a policy paper that will delineate the priorities and objectives for the EU to catch up with the US. Rightly, he focuses on prioritising basic research; however, he embraces industrial policy and protectionism. The EU’s track record on the former is terrible. As for the latter, it will prove difficult for a currency area that has both trade and current account surpluses to obtain any benefits from a trade war with China and the US.

The Butterfly Effect: Shocks from Afar

Very few people outside the Collateralized Loan Obligations market were familiar with Norinchukin Bank, a private bank owned by Japan’s 3,300 agricultural cooperatives, until it announced JPY1.5 trillion ($9.4 billion) in portfolio losses and plans to raise equity to fill that gap. Norinchukin Bank suffered the plight of Japan’s economic stagnation and private sector deleveraging as evidenced by a loans to deposit ratio of just 27.4%. Management decided to invest the excess liquidity in foreign bonds creating one of the largest carry trades anywhere. This is not a systemic bank in Japan, but it is a very large buyer of the highest rated tranches of CLOs. Will the bank’s appetite for CLO tranches diminish? Will this affect the funding cost for CLO structures? How will this affect the refinancing cost for Leveraged Buyouts? Will Norinchukin’s woes turn out to be the source of a butterfly effect that results in a tsunami thousands of miles away?

Can the euro actually be undone?

Many people will soon conclude that life before the euro was better in France, Italy, and other countries. The question is whether it would be possible to unwind the currency board union without causing major havoc in financial markets and taking down many banks.

Some analysts have argued that, as G7 member countries, France and Italy would have the right to redenominate their government debt without triggering a default, but this remains a highly complex legal issue. The prevailing legal consensus is that such a move would likely be considered a default under international law and financial norms. This is because government bonds are typically issued under terms that specify repayment in euros, so a unilateral change in the currency of repayment would alter the fundamental terms of the debt contracts.

Other analysts have advocated, at times of euro stress in the past that the core countries would leave the euro, as this would minimize the friction of a euro break up.

We are not advocating that there will be a break-up of the euro. However, we are positioning for additional market stress.

How to position

The first order effect is a weaker euro and lower valuations for banks because of higher volatility in bond portfolios and expectations of rate cuts. This will likely take place in sync with a flattening of the euro swaps curve.

We also have an FX position with a negative carry of 25 bps/year, which in the admittedly unlikely event of a euro break up should pay off 30%+.

Have a positive monday Luis! 😅